2018 was a year to forget for stockmarkets as they declined globally, with the UK’s FTSE100 one of the worst performers – see chart. UK residential property was a mixed bag with small gains at the national level balanced by a fall in London.

But Secured Development Funding provided handsome returns in 2018. In fact, as shown in the 5-year chart, this asset class has delivered consistent long-term returns with low volatility. This is why this asset class is a growing part of my portfolio.

Whether you invest independently, or via investment professionals (eg your pension fund), four asset classes which have traditionally dominated your investment menu: Equities (funds, stocks), Fixed Income (bonds), Property (to let) and Cash (in the bank).

The good news for investors is that now, access to a more effective asset class has become mainstream. One that delivers better returns with more consistency and low volatility.

Investing in Secured Development Funding was previously only available to banks or institutional investors (who might have let their wealthiest clients have a piece of the pie). Today, with Peer-to-Peer (P2P) investing becoming mainstream through technology and online platforms, anyone can access an asset class which delivers higher returns with less risk.

What is Secured Development Funding?

Very simply, it is funding required to build new homes in the UK. It generally consists of either secured debt (the focus of this article) or equity funding, with the latter enabling investors to share in the profits of development projects but without any asset-backed security.

Until recently the only providers of such funding have been the banks or institutional lenders. But things have changed, particularly with the emergence of Crowdfunding and P2P lending platforms, making the space more accessible for private investors looking for a better alternative to traditional asset classes – particularly with interest rates being so low.

[This article mainly focuses on Secured Development loans. Investing into the project’s equity offers higher projected returns and higher risk. At InvestLikeAPro, we recommend diversifying your portfolio with loans (debt) and equity].

This article explains 10 reasons why now is the time to make Secured Development funding a major part of your portfolio …

1. Better Returns and more Consistent Performance

Very simply, Secured Development Funding has performed better than other asset classes. In the short and long term. The two charts below say it all …

The stand-out performer is Secured Development Funding with better returns and consistency. As evident from the two charts, consistency is a quality that is rare amongst traditional asset classes.

Secured Development Funding is still below the radar for many people – mainly because IFAs and other distributors don’t make commissions like when selling traditional funds. But the performance record clearly shows it to be an asset class that investors cannot afford to ignore.

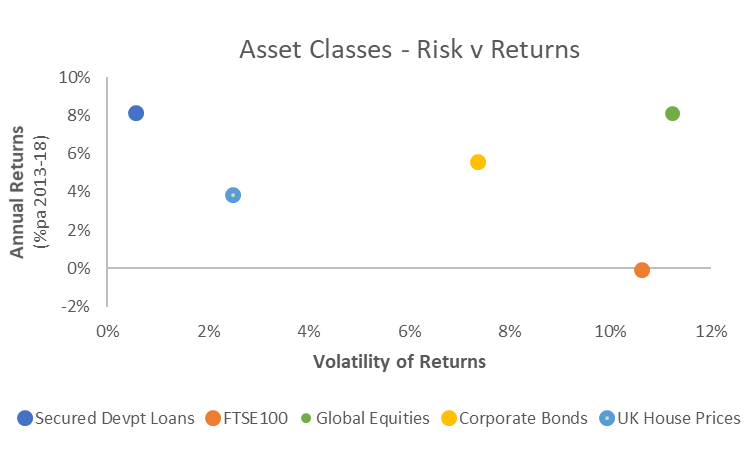

2. Lower risk – Secured Development funding has challenged the usual risk/return relationship

For most asset classes, risk and return are linked together – obtaining higher returns usually means having to take on higher risk – defined by the volatility of returns.

This can be seen from the chart below: over the last 5 years global equities have given higher returns but with higher risk. Compare this to corporate bonds which have seen lower returns for lower risk. UK housing is further down on the usual risk/return trade-off.

But there are 2 outliers which have defied the usual risk/return relationship: Secured development Loans had the lowest risk but highest returns whilst UK equities (FTSE100) had high risk and lowest returns!

Based on these risk/return numbers, UK equities are to be avoided whilst Secured Development Loans has to be a slam-dunk investment choice. Particularly if one expects interest rates to stay low.

And during a recession? What about performance in 2008, i.e. during the worst recession in living memory? The FTSE100 lost 31%, Global equities declined 40%, but UK house prices (as a proxy for the P2P/secured development sector which was then in its infancy) held up relatively well, dropping by 16%.

3. Built-in Downside Protection

Which other asset classes protect your capital after a market correction? Secured Development Funding comes with a free insurance policy – built-in downside protection. This is a huge advantage that very few other asset classes offer.

Secured Development funding is unique in including real security backing (UK bricks & mortar) that protects investor capital, should the market decline.

Say a development site has an (independent RICS) valuation of £1.5m. A senior loan of £1m is required for further development of the site. The loan-to-value (LTV) in the deal is therefore 67% with the equity cushion for lenders amounting to £0.5m, or 33%. So, as is typical, the amount of security exceeds the amount invested.

Now, let’s say the market has a 20% correction, as shown in the chart below …

As a result, the LTV rises to 83% and the equity cushion falls to £0.2m. Despite the correction the senior lender (investor) still has sufficient cushion to entirely recover their initial investment and potentially some interest earnings too.

This illustrates how the built-in insurance within Secured Development Funding generates consistently solid returns, with limited risk.

4. Due Diligence (DD) enables Consistent Returns

In this space, simply chasing the highest advertised returns is not advisable. To achieve consistently good returns, we have to select the right projects whilst avoiding the dogs.

This is where a solid DD process helps to de-risk opportunities. At InvestLikeAPro we have many years of investment DD behind us and our multi-layered process is rigorous (see our previous articles on www.investlikeapro.co.uk).

A good DD process includes:

- DD on the developer

- Track Record analysis

- Assessment of the developer’s process

- The developer’s team

- Their approach to risk management

- Legal agreements

- Detailed DD on the Project

- Planning Outcomes

- Breakdown analysis of projected development costs, sales and profits

- Multiple exit strategies

- Analysis of local liquidity, supply/demand, affordability conditions

- Stress testing and sensitivity analysis

- Risk Management and risk grading

- DD on the Security

- Fixed charge valuation analysis

- DD on the title(s)

- Corporate debentures (if any)

- Director Personal Guarantees (if any)

5. Returns do not require continued housing market gains

A common misconception is that returns will only be possible with housing market gains. Fortunately for investors, this is not the case. How many other asset classes still make handsome returns in the absence of market gains?

A flat market is good enough for the type of returns we expect and have seen. Indeed, as from the previous chart, even a 20% market correction offers security protection.

How can this be? As long there is a sound exit strategy at the end of the project that involves cashflow generation – and our DD would already have covered affordability for end-buyers, local supply/demand, the liquidity of the location/units, etc – the proceeds generated (assuming no market gains) will be sufficient to repay loan capital and interest.

The critical point is that returns are generated by DD and comfort around the execution of the development project and not from hope around market gains.

6. Low correlation with other asset classes

Correlation measures the extent to which different assets are linked, in terms of their returns.

The number ranges from -1 to +1 with -1 meaning two assets move in opposite directions (highly negatively correlated) and +1 means total synchronisation (high positive correlation).

When seeking to effectively diversify amongst different investments, we should look to combine assets which have low correlations – i.e. not close to +1 or -1. This will result in an overall portfolio with reduced risk.

![]()

The table above shows correlations for the different asset classes over the last 5 years. As you might expect, there is high correlation between Global Equities and the FTSE100 (0.94) and reasonably high vs Corporate Bonds.

But there is fairly low correlation between Secured Development Funding and UK house prices (0.40). This confirms what we said in the previous section about not needing house price gains.

Overall, Secured Development Funding has very low correlation with most asset classes, making it an excellent diversifier resulting in lower portfolio risk.

7. Diversification amongst Secured Loan Investments

Effective diversification is now easier than ever, with the proliferation of various P2P platforms. Once your DD is done, Secured Development Loans can easily be diversified amongst numerous projects. We know this is key to lowering risk, and hence investment success.

At InvestLikeAPro we recommend investing into 10-20 projects to create an effectively diversified portfolio.

Proper diversification takes several dimensions to create a balanced portfolio. Diversify on numerous levels including:

- The number of developers with whom you invest

- By geography (be exposed to numerous cities/regions)

- By sector (residential, office, retail, hospitality)

- By risk-type – equity and debt

- The underlying risk-source: eg new build-outs, conversion projects

Illustration of a diversified and balanced Portfolio – including an Equity allocation

The portfolio weights shown represent an evenly balanced portfolio. Each bucket shows typical expected returns and our risk grading score. This is not a recommendation, the above is for illustrative purposes only.

8. No hidden fees

Unlike with traditional funds, investing in development funding carries no additional hidden fees that eat into your wealth. The advertised return rate is what you get.

Of course, this assumes that loans do not default. However, the performance numbers shown above for Secured Development Funding are shown net, i.e. already including any defaults during that time period. With our rigorous DD process and the security backing (i.e. the insurance policy discussed above) we expect actual net defaults to remain low.

9. Easy to Monitor

Post investment, monitoring is easy. At InvestLikeAPro, we have a systematic monitoring system that requires monthly progress data from developers and the project. We are especially focused on the latest updates around Costing, Gross Development Value (GDV) and local pricing dynamics and Project Timeframe performance. Upon gathering the data, we update investors accordingly on each project.

Investment duration varies but usually range from 6 months up to 24 months. Our preference is to invest in projects with an average duration level of 12 months. And 18 months is normally the absolute maximum timeframe we feel comfortable with.

10. Easy investment access and tax-efficient wrappers

Technology and the new P2P and Crowdfunding platforms have increased choice for investors wishing to access this space.

Investment can now be made in various wrappers to maximise tax efficiency. Including ISAs (specifically, IFISAs), in a SIPP and also SSAS.

Manish Kataria

Founder, InvestLikeAPro

Join our Investor Circle to receive insights, resources and education – free and exclusive to members.

You’ll be the first to receive new investment insights and helpful ideas on how to build your capital and invest like a pro. All in a risk-managed and diversified manner.

Sign up at www.investlikeapro.co.uk

Manish Kataria CFA is a professional investor with 18 years’ experience in UK real estate and equity portfolio management. He has managed money for JPMorgan and other blue chip investment houses. Within real estate, he invests in and owns a range of UK property including developments, HMOs, serviced accommodation and BTLs.

")